Hospitalists are earning a little more, working a little harder, and are less likely to switch jobs or careers, according to the 2011 State of Hospital Medicine report. The annual report, based on data collected jointly by SHM and the Medical Group Management Association (MGMA), offers more than 10,000 compensation and productivity data points for all types of hospitalists, including, for the first time, an exclusive look at academic hospitalists.

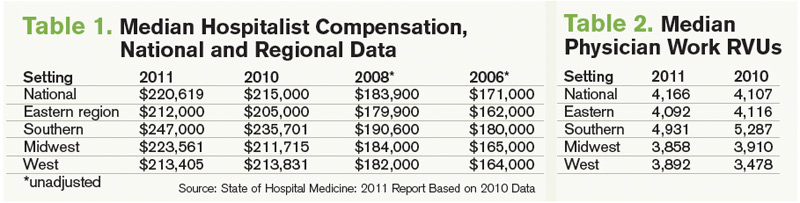

As previously reported, median adult hospitalist compensation increased to $220,619, a 2.6% increase from the $215,000 figure reported last year. “I think that’s a reflection of the market and demand for hospitalists, and the value that hospitals and other healthcare payors see that hospitalists bring,” says William “Tex” Landis, MD, FHM, medical director of Wellspan Hospitalists in York, Pa., and chair of SHM’s Practice Analysis Committee.

The compensation increases for hospitalists reported in the SHM-MGMA survey mirror results in other recent surveys. The 2011 Medical Group Compensation and Financial Survey, produced by the American Medical Group Association, found the overall average increase in physician compensation was 2.4%. Primary-care physicians (PCPs) reported a 2.6% increase in 2010, while the “hospitalist-internal medicine” category saw one of the steepest increases at 6.29%, according to the report (www.amga.org).

According to the 2011 MedScape Physician Compensation Report, 27% of the more than 15,000 physicians surveyed said their income increased from 2009 to 2010, whereas 50% said they saw no change. About 23% reported a decline in income, the report showed (www.medscape.com/features/slideshow/compensation/2011/).

click for large version

click for large version

Continuing a decadelong trend, the SHM-MGMA report shows hospitalists in the South make the most (median compensation $247,000, up from $235,701 in 2010) and hospitalists in the East ($212,000, up from $205,000 in 2010) lag behind the other regions (see Table 1).

The Hospitalist spoke to five members of SHM’s Practice Analysis Committee (PAC) about the survey results, and each points to continued nationwide demand as the driver of increased compensation. However, the committee also cautions HM groups and directors to be leery of trending this data, as the report is based on a volunteer survey, the survey population changes year to year, and only two years of identical survey data are available.

“As hospital medicine continues to grow, the hospitals become so dependent on the services that the hospitalists provide,” says PAC member Scarlett Blue, RN-BC, MSN, NE-BC, CPHQ, vice president of quality and clinical development for Eagle Hospital Physicians. “[Hospitals] know HM is critical and…I think that hospitalists demonstrate tremendous value, which the hospitals and the management groups recognize.”

The 2011 report, available Sept. 14, compiled data about 4,633 hospitalists in 412 groups. Eighty-five percent of the respondents classified themselves as “adult” hospitalists, 5% as “pediatric” hospitalists, and 10% as both adult and pediatric. Of note, this is the first time SHM has produced compensation and productivity data in consecutive years. In addition to compensation, the survey provides drill-down capability on productivity and reimbursement metrics, along with specific data regarding night coverage arrangements (see “Survey Insights,”), financial support payments, physician turnover, and, for the first time, a look at nonphysician providers (NPPs) in HM practice (see “Nonphysician Provider Data Available for First Time,”).

continued below…

Nonphysician Provider Data Available for First Time

Blue

Hospitalist groups were asked about nurse practitioner (NP) and physician assistant (PA) employment, and 49% of HM groups reported having some type of nonphysician provider (NPP) on staff (see Figure 4). Those results, although not startling to some, should open the other half’s eyes, Dr. Landis says.

“Just looking to the future, I think most of us can see physician extenders¬⎯NPs and PAs⎯becoming more and more important in the delivery of hospital care,” he says. “We’re going to be looking to get more information about how that’s happening and what functions they’re performing and what resources, financially and otherwise, are required to help them be effective team members.”

Hawley says NPPs are a critical part of HM’s future but admits some hospitalists still are reluctant to work with NPPs because compensation and incentives are misaligned. “Oftentimes what a [physician] compensation plan will do is not provide for any work that is being done by the NPP,” she says. When physicians find out they also are being measured on patient satisfaction and other metrics, “then the NPP becomes very, very critical. So we’re seeing more and more acceptance. Our opinion, as a consulting group, is that there won’t be a [HM] program in this country that doesn’t somehow use nonphysician providers. There just aren’t enough hospitalists to go around.”

Dr. Landis says his committee is planning to collaborate with SHM’s Nonphysician Provider Committee to determine the best way to collect and disseminate NPP benchmarks. “That’s a future trend and everybody can see it,” he adds. “We have yet to solidify, though, how we’re going to measure and evaluate what’s going on there.” —JC